Crude and Refined Products Price Review and Outlook

The geopolitical escalations in the Middle East have placed significant pressure on the global energy supply chain, reflecting the sector’s high level of integration and volatility. The region accounts for nearly one-third of global crude oil supply and about 48% of the world’s proven crude reserves. In particular, the Strait of Hormuz facilitates the transit of approximately 20% of global crude oil supply. Given the strategic importance of the region in global oil production, the war has significantly disrupted supply flows and triggered sharp increases in international crude oil prices since early March.

Crude oil prices rose to their highest levels since the 2022 Russia-Ukraine war following the escalation of hostilities involving the US, Israel, and Iran. The retaliatory attacks across several Gulf states triggered an unprecedented surge in crude prices to about USD130 per barrel. Tragically, the war also led to the partial closure of the Strait of Hormuz and attacks on critical energy infrastructure, including Iran’s South Pars gas field, Saudi Arabia’s Shaybah oil field, and the UAE’s Shah gas field.

As a result of the war, international crude oil prices remain above USD100 per barrel despite the ceasefire agreement, which remains highly fragile. Current crude prices remain about 79.12% higher than levels recorded in January, notwithstanding a marginal decline of 1.31% in the current pricing window. According to the International Energy Agency (IEA), global oil demand is projected to contract by 80 kb/d this year, largely due to supply constraints and elevated prices.

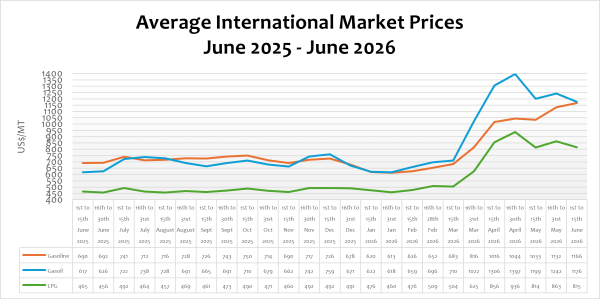

Consequently, refined petroleum product prices have experienced significant volatility. Petrol prices on the international market increased by 3.04%, while diesel, LPG, and ATK declined by 3.35%, 5.53%, and 6.65%, respectively. On a year-on-year basis, petrol, diesel, and LPG prices have risen by 68.97%, 90.55%, and 73.34%, respectively. Compared to the beginning of the year, prices have surged by 88.08% for petrol, 89.08% for diesel, and 71.39% for LPG.

In addition to rising global prices, freight and insurance costs have increased sharply due to prevailing security concerns in the Middle East, significantly affecting vessels transporting petroleum products to Sub-Saharan Africa. As a result, pump prices for petrol are expected to increase, while diesel prices may decline marginally during the pricing window of 1st to 15th June 2026.

FuFeX30 and Spot Rates

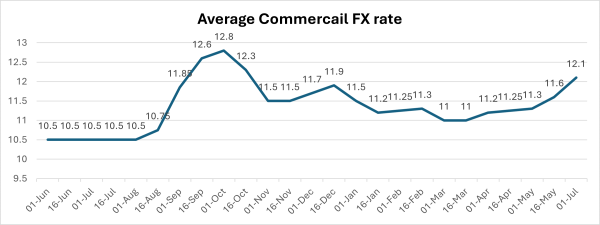

The Fufex30[1] for the first selling window of June (1st to 15th June 2026) is estimated at GHS12.1000/USD, based on quotations received from oil-financing commercial banks. Moreover, the applicable spot rate for cash sales is estimated at GHS11.9000/USD because of the recent pressure on the demand for USD. The cedi is currently depreciating due to concerns of liquidity for the importation of petroleum products. The Chamber is currently in engagements with the BOG to improve FX supply for BIDECs.

[1] The Fufex30 is a 30-day GHS/USD forward FX rate used as a benchmark rate for BIDECs ex-ref price estimations.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 1st to 15th June 2026

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 1166.0800 | 1175.9500 | 815.2300 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 150 | 250 | 270 |

| Spot FX Rates | 11.9000 | 11.9000 | 11.9000 |

| FuFex30 (GHS/USD) | 12.1000 | 12.1000 | 12.1000 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 11.8244/ltr | 14.3387/ltr | 12.9142/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 12.0231/ltr | 14.5796/ltr | 13.1313/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

During the 16th to 31st May 2026 selling window, total taxes, levies, and regulatory margins accounted for approximately 28.92%, 25.71%, and 13.15% of the ex-pump prices of petrol, diesel, and LPG, respectively. This was partly due to the government’s suspension of some margins and levies on diesel by about GHS1.07/Ltr in the window under review to provide relief for consumers transporters.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) | LPG (GHS/KG) |

| ENERGY SECTOR SHORTFALL AND DEBT REPAYMENT LEVY | 1.95 | 1.93 | 0.73 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.0 | – |

| BOST MARGIN | 0.12 | 0.0 | – |

| FUEL MARKING MARGIN | 0.09 | 0.0 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.90 | 0.30 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 4.27 | 3.18 | 2.11 |

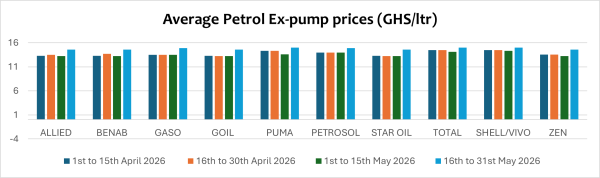

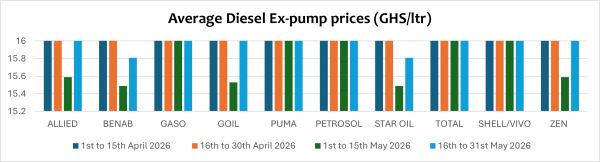

OMC Pricing Performance: 16th to 31st May 2026

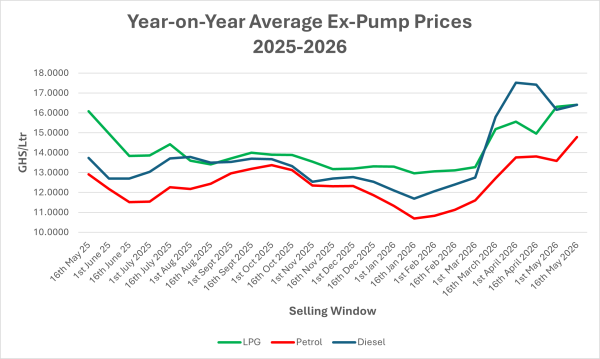

Petroleum product pump prices have been high since the escalations of the geopolitical tension in the Middle East involving the US, Israel and Iran. The geopolitical escalation has had a very significant impact on global energy prices, particularly crude oil and petroleum products. Since the escalation in March, crude oil prices at the international market have risen significantly to their highest since the unusual surge in prices experienced in 2022 when the Russia-Ukraine war commenced. Crude oil price rose from an average of USD67.40/bbl in February to as high as USD129/Bbl in April when the escalations were at their peak. Due to the current negotiations on the truce agreement, crude oil prices have currently slumped slightly to an average of USD110.59/Bbl.

Moreover, due to the insecurities in the Middle East, particularly in the Strait of Hormuz, there has been an unprecedented surge in freight and insurance costs globally. Demurrage cost has also increased exorbitantly, mainly due to the geopolitical escalations and the disruptions in global crude production.

Consequently, pump prices of petroleum products have increased significantly since the escalations began in the first window of March. Pump prices rose afterwards to historical highs comparable to the heights reached in November 2023 when the cedi depreciated significantly. In effect, diesel pump prices rose to about GHS18 per litre at some Retail Outlets.

Following the significant surge in pump prices, government suspended some margins and levies on petrol and diesel for a period of one month beginning from the second window of April to provide respite to consumers. After the one-month period, government restored all the margins on petrol but rather partially restored some of the margins on diesel. This intervention aimed at cushioning consumers from the significant escalation in pump price, similar to the reliefs provided by some European countries, including Germany, Italy, Poland, and Hungary, to provide relief for consumers.

Following the significant surge in pump prices, government suspended some margins and levies on petrol and diesel for a period of one month beginning from the second window of April to provide respite to consumers. After the one-month period, government restored all the margins on petrol but rather partially restored some of the margins on diesel. This intervention aimed at cushioning consumers from the significant escalation in pump price, similar to the reliefs provided by some European countries, including Germany, Italy, Poland, and Hungary, to provide relief for consumers.

In the window under review, petrol pump prices rose by 8.81%, mainly due to the increase in international prices and due to the restoration of the margins and levies (GHS0.36) previously suspended by government. On a year-to-date basis, pump prices have cumulatively increased by about 30.41%, reflecting sustained cost pressures within the downstream petroleum market.

Diesel pump prices also increased by 2.34% due to the increase in pump prices and the recent pressure on the Ghanaian cedi. On a year-to-date basis, diesel prices have gone up by 36.66% despite the intervention by government.

In the coming window of 1st to 15th June 2026, petrol is expected to rise by 6.28%, while diesel is expected to decline slightly by 1.11% due to the combined effect of international price movements and the performance of the cedi.