Crude and Refined Products Price Review and Outlook

International crude oil prices have begun to surge again following pockets of incidents and attacks between the US and Iran around the Strait of Hormuz, raising concerns over potential supply disruptions in the global oil market. According to Reuters News, “U.S. President Donald Trump said on Monday that ceasefire talks with Iran were on ‘life support,’ pointing to disagreements over Tehran’s demands of a cessation of hostilities on all fronts, the removal of a U.S. naval blockade, the resumption of Iranian oil sales and compensation for war damage.”

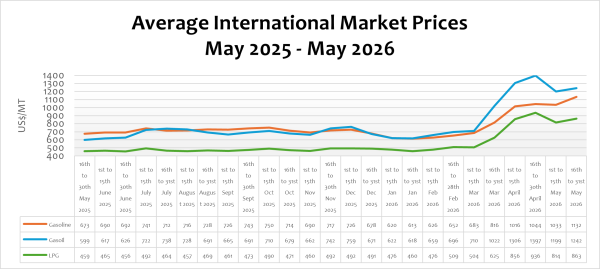

Although crude oil prices rose significantly to about USD130/Bbl in April due to the escalation of the war between US/Israel and Iran, prices subsequently fell by about 12.33% in the first window of May due to the ceasefire agreement. However, prices later surged again as hopes of sustaining the truce agreement in the Middle East dwindled amid pockets of incidents and renewed tensions in the region. As a result, crude oil prices in the window under review declined marginally by 1.52%. On a year-on-year and year-to-date basis, crude oil prices remain significantly higher by 78.20% and 81.52%, respectively.

As a result of the ongoing security concerns in the Middle East, coupled with the blockage of the Strait of Hormuz, refined petroleum products prices have been on the surge despite the marginal drop in crude oil prices. The international market price of petrol, diesel, and LPG rose by 9.58%, 3.60%, and 6.07, respectively, mainly due by the fragility of the ceasefire agreement in the Middle East. On a year-on-year basis, petrol, diesel, and LPG are up by 68.15%, 107.51%, and 88.12%, respectively. Compared to prices at the beginning of the year, petrol, diesel, and LPG have nearly doubled at 82.54%, 99.78%, and 81.42%, respectively.

According to the International Energy Agency (IEA), “Global oil supply plummeted by 10.1 mb/d to 97 mb/d in March, due to the attacks on energy infrastructure in the Middle East and ongoing restrictions on tanker movements through the Strait of Hormuz leading to the largest disruption in history”. According to the Agency, oil demand is expected to contract by 80 kb/d this year, mainly due to scarcity and higher prices.

In addition to the surging global prices, the cost of freight and insurance has surged globally due to the prevailing security concerns in the Middle East. This development has significantly impacted vessels transporting petroleum products to Sub-Saharan Africa. As a result of the rising refined petroleum products prices and surging premiums, pump prices are expected to rise in the coming window of 16th to 31st May 2026.

FuFeX30 and Spot Rates

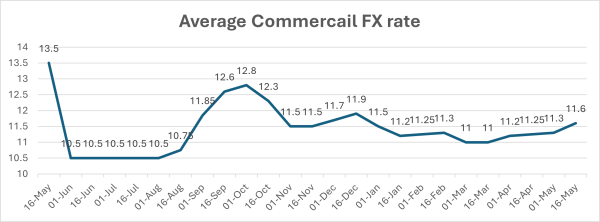

The Fufex30[1] for the second selling window of May (16th to 31st May 2026) is estimated at GHS11.6000/USD, based on quotations received from oil-financing commercial banks. Moreover, the applicable spot rate for cash sales is estimated at GHS11.4000/USD.

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 16th to 31st May 2026

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 1131.7300 | 1242.4800 | 862.9800 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 150 | 250 | 270 |

| Spot FX Rates | 11.4000 | 11.4000 | 11.4000 |

| FuFex30 (GHS/USD) | 11.6000 | 11.6000 | 11.6000 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 11.0319/ltr | 14.3771/ltr | 12.9160/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 11.2254/ltr | 14.6293/ltr | 13.1426/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

During the 1st to 15th May 2026 selling window, total taxes, levies, and regulatory margins accounted for approximately 28.79%, 13.93%, and 13.23% of the ex-pump prices of petrol, diesel, and LPG, respectively. This was partly due to the government’s reduction of some petroleum product margins as a relief for consumers. The data indicate that consumers continue to bear a substantial tax burden.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) | LPG (GHS/KG) |

| ENERGY SECTOR SHORTFALL AND DEBT REPAYMENT LEVY | 1.95 | 1.93 | 0.73 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRIMARY DISTRIBUTION MARGIN | 0.19 | 0.0 | – |

| BOST MARGIN | 0.09 | 0.0 | – |

| FUEL MARKING MARGIN | 0.07 | 0.0 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.66 | -0.63 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 3.91 | 2.25 | 2.11 |

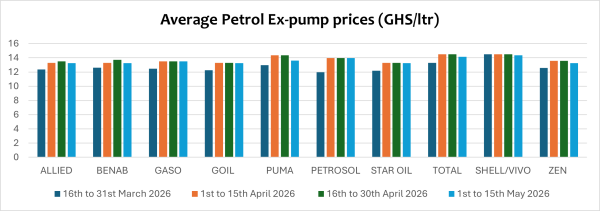

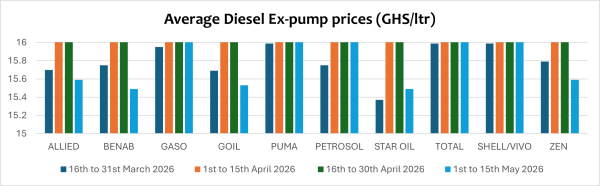

OMC Pricing Performance: 1st to 15th May 2026

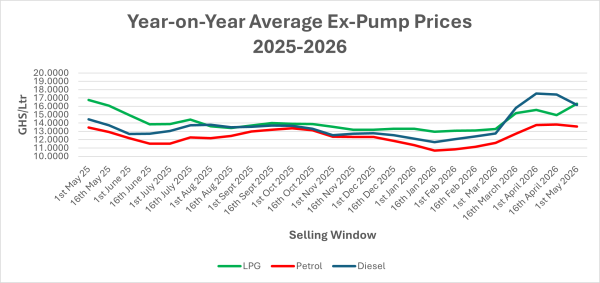

The prolong escalations of the geopolitical tension in the Middle East has had a very significant impact on global energy prices, particularly crude oil and petroleum products. Since the escalation in early March, international crude oil prices have increased to their highest since the unusual surge in prices experienced in 2022 when the Russia-Ukraine war commenced. Consequently, pump prices of petroleum products have increased for six consecutive pricing windows since February 2026, declining only in the 1st pricing window of May, despite the stability of the Ghanaian cedi within the period.

Following the significant surge in pump prices, which triggered several transport unions to consider fare increases , the government suspended some margins and levies on the petroleum products to provide respite to consumers. Specifically, the Primary Distribution Margin (PDM), BOST Margin, and Fuel Marking Margin (FMM) were fully suspended for diesel and reduced for petrol. This intervention resulted in a moderate decline in pump price in the window 2nd window of April, cushioning consumers from the significant escalation that was expected in the pricing window.

Some European countries, including Germany, Italy, Poland, and Hungary, have introduced funding measures, including fuel price caps and tax cuts, to provide relief for consumers.

There were no indications from government as to whether the suspension of these margins and levies would be extended into subsequent pricing windows, as the interventions were initially intended to last for a period of four (4) weeks, ending on 15th May 2026.

In the window under review, petrol pump prices declined slightly by 1.69%, mainly due to the stability of the cedi and the government’s removal of margins and levies, summing up to about GHS0.36 from the price of petrol. On a year-to-date basis, pump prices have cumulatively increased by about 19.89%, reflecting sustained cost pressures within the downstream petroleum market.

Diesel pump prices, however, decreased by 7.18% due to the significant cut in the government regulatory margins of about GHS2 per liter in the window under review, despite the significant surge in the international price. On a year-on-year basis, diesel prices are up by about 11.84% and have increased by 33.54% compared to January 2026 levels. However, Liquefied Petroleum Gas (LPG) recorded an increase of about 8.67%, largely reflecting movements in international market prices and partly because government did not remove or cut any of the margins and levies in the LPG Price Build-Up.

In the coming window, pump prices are expected to rise due to the combined effect of the rise in international prices and the slight depreciation of the cedi, coupled with the recent surge in the freight and insurance premiums due to the insecurity issues around the Middle East.