Crude and Refined Products Price Review and Outlook

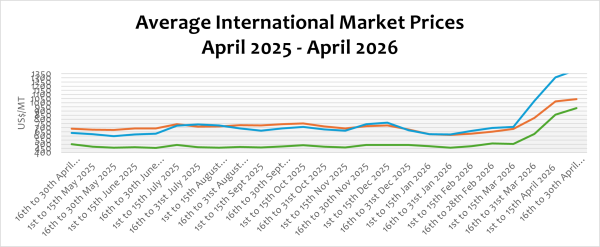

International crude oil prices surged to approximately USD130 per barrel in the first week of April, marking the highest level since 2022. This compares to the peak of about USD133 per barrel recorded in May 2022, following the onset of the Russia-Ukraine War, which significantly disrupted global energy markets.

Crude oil prices have surged significantly since January, increasing by approximately 110.24%, thereby more than doubling their levels recorded in December 2025. On a year-on-year basis, prices have risen by about 83.54%, reflecting the scale of the current market disruption. This sharp increase has been driven primarily by the escalating conflict involving the US and Israel against Iran, which has significantly heightened geopolitical risk in global energy markets.

The intensification of hostilities has resulted in missile strikes targeting key oil infrastructure, including production wells and refining assets. Notably, the South Pars Gas Field, located offshore in the Persian Gulf, was struck, prompting retaliatory actions that extended to liquefied natural gas (LNG) facilities in Qatar. According to Reuters, these retaliatory attacks are expected to reduce Qatar’s LNG export capacity by approximately 17%, equivalent to about 12.7 million metric tonnes over the next three to five years. This projected supply disruption is likely to have significant implications for energy markets, particularly in Europe and Asia.

Furthermore, the situation has been exacerbated by the closure of the Strait of Hormuz by Iran, alongside recent measures by the US to restrict vessels intending to access Iranian ports. The IMF and the World Bank have therefore cautioned countries from energy hoarding to mitigate the risk of a broader energy crisis.

In the downstream market, refined petroleum product prices have also surged, with petrol, diesel, LPG, and ATK increasing by 2.77%, 6.98%, 9.38%, and 1.21%, respectively. Relative to January levels, petrol, diesel, and LPG prices have surged by about 86.39%, 124.65%, and 96.83%, respectively.

However, ongoing diplomatic negotiations aimed at de-escalating the conflict could provide some relief to global energy markets, with the potential for price moderation before the end of the month.

FuFeX30 and Spot Rates

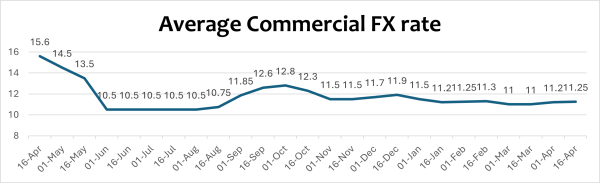

The Fufex30[1] for the second selling window of April (16th to 30th April 2026) is estimated at GHS11.2500/USD, based on quotations received from oil-financing commercial banks. Moreover, the applicable spot rate for cash sales is estimated at GHS11.1500/USD based on quotations from oil-financing commercial banks, representing a depreciation of 0.45%.

The graph indicates that although the Ghanaian Cedi appreciated significantly in 2025, continued fluctuations in its value still pose challenges to effective business planning. A stable and strong currency generates broad-based economic benefits, especially for the petroleum sector, where products are predominantly imported and highly exposed to exchange rate movements.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 16th to 30th April 2026

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 1044.0000 | 1397.1400 | 936.2800 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 120 | 1200 | 250 |

| Spot FX Rates | 11.15000 | 11.1500 | 11.1500 |

| FuFex30 (GHS/USD) | 11.2500 | 11.2500 | 11.2500 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 9.7989/ltr | 14.2941/ltr | 13.2270/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 9.8867/ltr | 14.4223/ltr | 13.3457/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

Total taxes, levies, and regulatory margins within the 1st to 15th April 2026 selling window accounted for about 31.04%, 24.26%, and 12.40% of the ex-pump prices of petrol, diesel, and LPG, respectively. This data shows that consumers are overburdened with levies on petroleum products.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) | LPG (GHS/KG) |

| ENERGY SECTOR SHORTFALL AND DEBT REPAYMENT LEVY | 1.95 | 1.93 | 0.73 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.26 | – |

| BOST MARGIN | 0.12 | 0.12 | – |

| FUEL MARKING MARGIN | 0.09 | 0.09 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.90 | 0.90 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 4.27 | 4.25 | 2.11 |

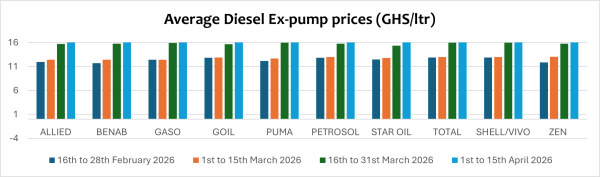

OMC Pricing Performance: 1st to 15th April 2026

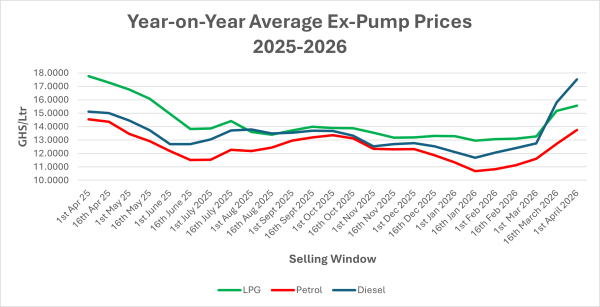

Pump prices of petroleum products have increased for the 6th consecutive pricing windows since February 2026, driven largely by escalating geopolitical tensions in the ongoing US/Israel-Iran war. While the Ghanaian Cedi has remained relatively stable since the second quarter of 2025, the upward pressure from rising international crude oil prices has translated into persistently higher ex-pump prices. This divergence between stable exchange rates and elevated global oil benchmarks continues to exert strain on domestic fuel pricing.

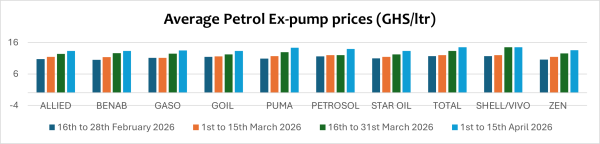

Currently, some Oil Marketing Companies (OMCs) are selling diesel at prices exceeding GHS18.00/Ltr, a level last observed in 2023 during a period of significant foreign exchange depreciation, when the cedi exceeded GHS18 to the US dollar. In response to the current price trajectory, transport unions have indicated potential increases in transport fares to reflect the rising cost of fuel at the pump.

The European Commission has permitted its members to provide relief to citizens in response to the surging pump prices. According to Reuters news agency, “the Commission on Monday proposed changing EU state aid rules to allow more public spending for industries hit acutely by fuel price increases, including agriculture, road transport and shipping within Europe”. These changes would let governments cover part of the price increase companies have paid for their fuel. Some countries, such as Germany, Italy, Poland , and Hungary, have already introduced funding measures, including fuel price caps and tax cuts, to provide relief for consumers.

The government of Ghana announced its plans to remove some selected taxes and margins from petroleum products to provide some relief to consumers and the transport sector in the coming window of 16th to 30th April 2026. This will help mitigate the impact of the rising pump prices, which has far-reaching impact beyond the transport sector to food security and inflation.

In the window under review, petrol pump prices increased by approximately 8.21%, driven by the combined impact of a depreciation in the Ghanaian Cedi and rising international petroleum product prices. On a year-to-date basis, pump prices have cumulatively increased by about 21.41%, reflecting sustained cost pressures within the downstream petroleum market.

Similarly, diesel pump prices increased by an average of approximately 10.89% during the review period, driven by exchange rate pressures and rising international product prices. On a year-on-year basis, diesel prices are up by about 20.30% and have increased by 44.78% compared to January 2026 levels. Liquefied Petroleum Gas (LPG) also recorded an increase of about 2.50%, largely reflecting movements in international market fundamentals.

Following government’s announcement to remove certain taxes and marketing margins on petroleum products, pump prices are projected to ease marginally in the next pricing window covering 16th to 30th April 2026.

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.