Crude and Refined Products Price Review and Outlook

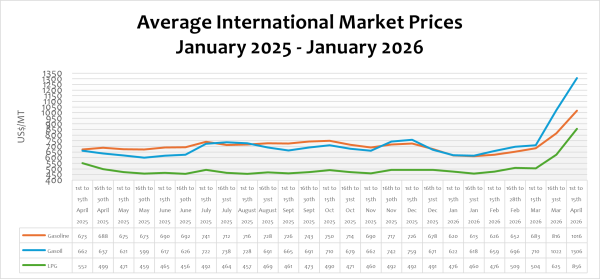

The price of crude in the international market has witnessed an unprecedented surge since 28th February, when the US and Israel jointly attacked Iran. Crude prices have since then escalated to their highest in years due to the continual attacks on oil refineries and other storage infrastructure within the Gulf region. Reuters News agency reported that in March 2026, Israeli forces struck Iran’s South Pars gas field, the world’s largest natural gas reserve, causing significant damage to processing facilities and triggering severe global energy market disruptions. In retaliation, Iran attacked Qatar’s Ras Laffan LNG export hub, causing significant damage. These actions further resulted in a significant escalation in oil prices.

Despite the decision by the International Energy Agency (IEA) and the G7 countries to release a record volume of oil stockpiles to help mitigate potential supply disruptions, and the OPEC nations also announcing to increase production from April, crude prices are still on the rise. Particularly, crude oil prices surged reaching approximately US$120/bbl at the peak of the tensions before moderating to an average of US$109.66/bbl, representing a year-on-year increase of 51.11% and a year-to-date increase on about 77.62% mainly from the ongoing war.

Moreover, refined petroleum products prices, petrol, diesel, LPG, and ATK have almost doubled since the beginning of the war. On a year-to-date basis, petrol, diesel, LPG, and ATK are up by 63.86%, 109.99%, 79.97%, and 136.86%, respectively. This shows that prices at the pumps in the coming window are expected to be double the pump prices in January.

Notwithstanding, the expectations of an imminent cease fire, the current blockage of the Strait of Hormuz, the persistent attacks on oil vessels at the Strait and the disruptions at the Qatar’s biggest LNG terminal, international prices are expected to remain on the high. According to Qatari authorities the destruction of the LNG facility will take about 5 years to repair. In addition to these, the geopolitical crises have also raised the risk premiums, as well as insurance and freight cost to significant highs resulting in many ships having to change their shipping routes. Reuters News agency reported that at least 11 tankers had to divert route from Europe to Asia due to the tightening supply in Asia.

FuFeX30 and Spot Rates

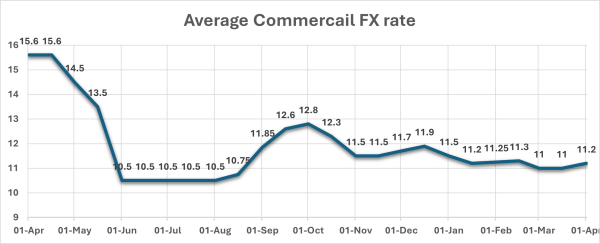

The Fufex30[1] for the first selling window of April (1st to 15th April 2026) is estimated at GHS11.2000/USD, based on quotations received from oil-financing commercial banks. Moreover, the applicable spot rate for cash sales is estimated at GHS11.0000/USD based on quotations from oil-financing commercial banks, representing a depreciation of about 2%.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 1st to 15th April 2026

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 1015.9100 | 1305.9800 | 855.9800 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 150 | 150 | 250 |

| Spot FX Rates | 11.0000 | 11.0000 | 11.0000 |

| FuFex30 (GHS/USD) | 11.2000 | 11.2000 | 11.2000 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 9.6829/ltr | 13.5334/ltr | 12.1658/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 9.8590/ltr | 13.7794/ltr | 12.3870/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

Total taxes, levies, and regulatory margins within the 16th to 31st March 2026 selling window accounted for about 33.59%, 26.90%, and 14.21% of the ex-pump prices of petrol, diesel, and LPG, respectively. This data shows that consumers are overburdened with levies on petroleum products.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) | LPG (GHS/KG) |

| ENERGY SECTOR SHORTFALL AND DEBT REPAYMENT LEVY | 1.95 | 1.93 | 0.73 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.26 | – |

| BOST MARGIN | 0.12 | 0.12 | – |

| FUEL MARKING MARGIN | 0.09 | 0.09 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.90 | 0.90 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 4.27 | 4.25 | 2.11 |

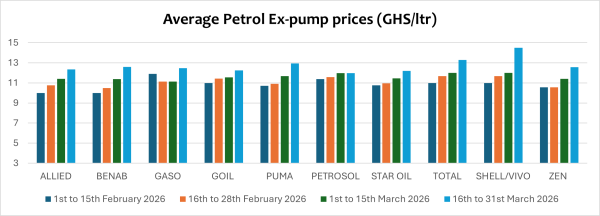

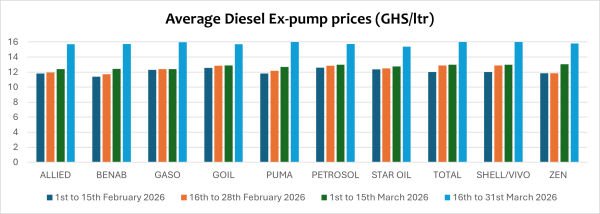

OMC Pricing Performance: 16th to 31st March 2026

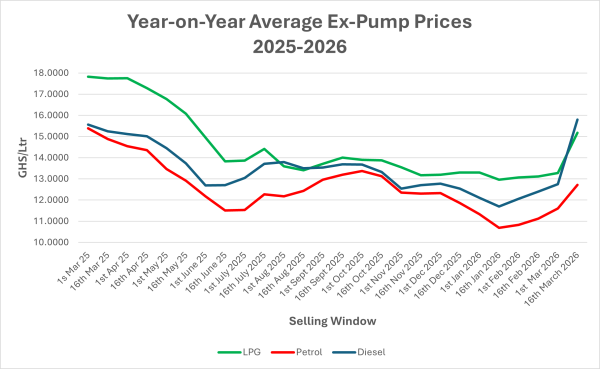

Petroleum products pump prices are at their highest in 9 months, rising back to the days when pumps crossed GHs15 to a liter. Pump prices of petroleum products in Ghana have been on a downward decline since around April 2025, largely driven by the appreciation of the Ghana cedi and declining international prices of crude oil and refined petroleum products. These developments translated into lower ex-pump prices across several pricing windows, with petrol falling below GHs10/Ltr and diesel below GHs12/Ltr at some retail outlets in January 2026. The sustained reductions provided notable relief to consumers, contributed to a decline in transport fares, and helped ease the inflationary pressures within the economy.

However, developments in the global oil market have exerted upward pressure on domestic fuel prices, rising between 10% to 23% in the window under review. The geopolitical escalations in the Middle East have pushed international crude oil prices to their highest since 2022. These global events and the resultant volatilities in the global market are passed on directly to African countries due to their heavy reliance on imported refined products, despite the fact that Africa produces about 10% of global crude.

In the window under review, pump prices of petrol rose by about 9.60% due to the surge in international prices arising from the escalating US/Israel and Iran war in the Middle East, which has escalated to the Gulf countries. On a year-on-year basis, pump prices of petrol are down by about 14.63%. However, pump prices are up by about 12.20% compared to January of this year.

Similarly, pump prices of diesel also rose by an average of about 23.86% in the window under review due to similar factors. Compared to the same period last year, pump prices of diesel are up by 3.60% and 30.55% since January 2026. LPG, however, rose by 14.14% due to international market factors.

In the coming window of 1st to 15th April, pump prices are expected to experience further upward adjustments if geopolitical tensions persist and international crude prices remain elevated. However, market analysts indicate that any significant increase may be moderated if major oil-producing countries increase supply or release strategic reserves to stabilize the global oil market.

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.