Crude Oil and Refined Products Market Review and Outlook

Notwithstanding the recent surge in global crude prices, the average crude price fell by about 7% in Q1 2024 compared to Q4 2023. Recent data has shown an upsurge in the price of crude oil reaching as high as USD85.44/bbl since November 2023. Compared to the same period last year, crude oil prices have risen by about 14%. This surge is attributed to higher-than-expected economic growth, reduced interest rates in Europe and the US, and the most recent geopolitical upheavals (Houthi attacks on Red Sea shipping) in the Middle East affecting the shipment through the Red Sea. According to Reuters, “Oil prices will gain some momentum this year as demand picks up and output curbs by the OPEC+ producer group continue to squeeze supply that is already being pressured by military conflicts”.

In line with this, while OPEC+ has projected global demand to grow by about 2.25 million bpd this year, the IEA project demands to grow by about 1.3 million bpd, driven largely by increased crude demand in India, China, and the US. Nevertheless, OPEC+ is expected to continue to underproduce to maintain high prices.

These events, coupled with the recent attacks on Russian oil refineries by Ukraine and the surging demand for crude and petroleum products in China, are expected to maintain crude and petroleum products prices higher in Q2 2024. Notwithstanding the production cut by OPEC+ countries, supply might remain uninterrupted, given the IEA’s indication that global production will surge by about 1.7 mb/d to a record 103.8 mb/d in 2024, with some non-OPEC+ countries (United States, Guyana, Brazil, and Canada) contributing about 95% of the increment.

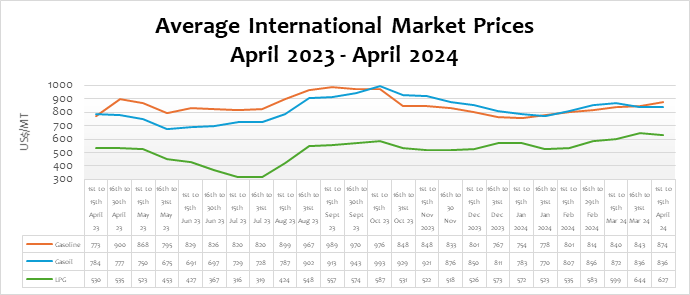

The international prices of diesel and LPG declined by 0.09% and 2.58%, respectively, while petrol rose by about 3.57%. Compared to the same period last year, petrol, diesel, and LPG prices rose by 13.11%, 6.59%, and 18.34% respectively. On a year-to-date basis, the international market price of petrol, diesel, and LPG surged by 15.97%, 6.95%, and 9.59%, respectively.

FuFeX30 and Spot Rates

The Fufex30[1] for the first selling window of April (1st to 15th April 2024) is estimated at GHS13.8500/USD, while the applicable spot rate for cash sales is GHS13.5500/USD based on quotations received from oil financing commercial banks.

| SUMMARY REPORT OF BANK OF GHANA FX AUCTIONS TO BIDECs | ||

| Window | Percentage Offered | Auction FX Rate (GHS/USD) |

| 1st to 15th December 2023 | 19% | 11.9131 |

| 16th to 31st December 2024 | 29% | 12.1512 |

| 1st to 15th January 2024 | 19% | 12.1497 |

| 16th to 31st January 2024 | 31% | 12.1369 |

| 1st to 15th February 2024 | 21% | 12.3948 |

| 16th to 29th February 2024 | 23% | 12.4888 |

| 1st to 15th March 2024 | 23% | 12.7291 |

| 16th to 31st March 2024 | 22% | 12.9737 |

The BoG’s bi-weekly FX auction to BIDECs in the 16th to 31st March 2024 pricing window for the purchase of petroleum products was US$20 million, representing 22% of BIDECs’ bid. The FX rate at which the BoG auctioned to BIDECs was GHS12.9737/USD, representing a depreciation of 1.89% compared to the previous window’s rate. The BOG auction rate has depreciated by about 6.78% from the beginning of the year and about 11.05% from November 2023 to April 2024.

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window, and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

(International Market Price+ CBOD Benchmark Premium) × Fufex30/Spot FX

=

Conversion Factor

Ex-ref Price Effective 1st to 15th April 2024

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 874.0900 | 835.6400 | 627.3000 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 120 | 120 | 260 |

| Spot FX Rates | 13.5500 | 13.5500 | 13.5500 |

| FuFex30 (GHS/USD) | 13.8500 | 13.8500 | 13.8500 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 10.1698/ltr | 10.9419/ltr | 12.0229/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 10.3950/ltr | 11.1841/ltr | 12.2891/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

Total taxes, levies, and regulatory margins within the 16th to 31st March 2024 selling window accounted for 24.6%, 22.8%, and 15.0% of the ex-pump prices of petrol, diesel, and LPG, respectively.

The Ministry of Finance through the Ministry of Energy has directed to National Petroleum Authority to remove the Price Stabilisation and Recovery Levy (PSRL) from the Price Build-Up for a period of three months (1st April to 30th June 2024). The removal of the PSRL from the Price Build-Up will partly reduce the escalating pump prices and insulate consumers within the period.

| TRM Components | Gasoline (GHS/ltr) | Gasoil (GHS/ltr) | LPG (GHS/KG) |

| ENERGY DEBT RECOVERY LEVY | 0.49 | 0.49 | 0.41 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRICE STABILISATION & RECOVERY LEVY | 0.16 | 0.14 | 0.14 |

| SANITATION & POLLUTION LEVY | 0.10 | 0.10 | – |

| ENERGY SECTOR RECOVERY LEVY | 0.20 | 0.20 | 0.18 |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.26 | – |

| BOST MARGIN | 0.12 | 0.12 | – |

| FUEL MARKING MARGIN | 0.09 | 0.09 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.85 | 0.85 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 3.22 | 3.20 | 2.11 |

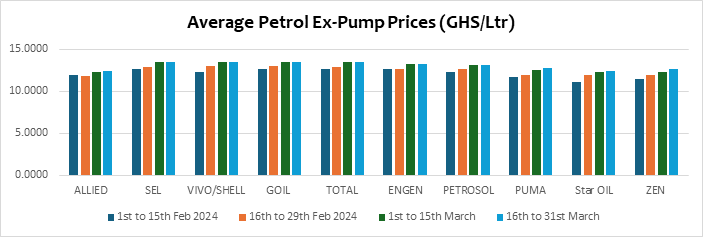

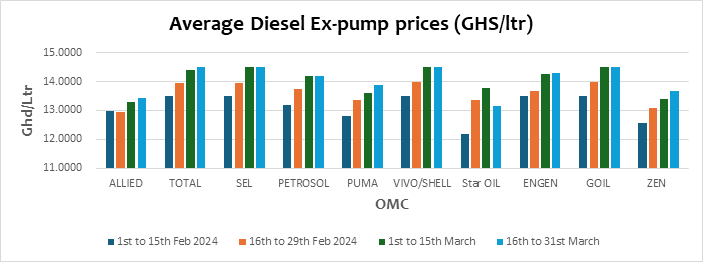

OMC Pricing Performance: 16th to 31st March 2024

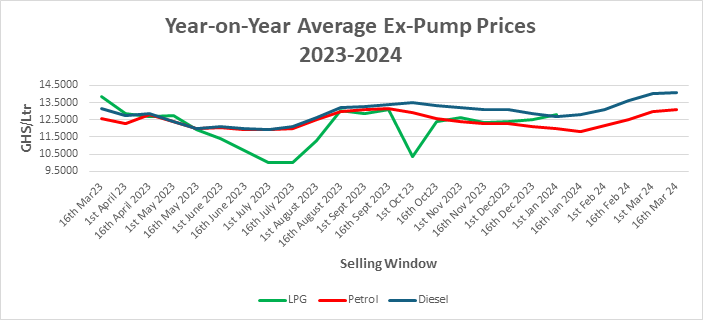

The average pump prices of petroleum products for the 16th to 31st March 2024 (the second pricing window of March) surged by an average of 0.6%, 0.2%, and 0.5% for petrol, diesel, and LPG, respectively. This rise is primarily attributed to the sharp depreciation of the Cedi against the US dollar within the February 27th to March 11th international pricing window. At the global level, prices of crude and petroleum products continue to rise due to increasing global demand and supply bottlenecks.

The Ghanaian Cedi has risen over a difference of GHS1.00 against the USD since January this year, this has impacted the pricing of petroleum products, which has also risen by about USD120/MT and USD50/MT for petrol and diesel, respectively, since January.

Pump prices of petrol have risen by 0ver 40% since March 2022 and by over GHS1/Ltr since January 2024. The Pump price of petrol, which averaged GHS9.3390/Ltr is currently being quoted at about GHS13.4900/Ltr by some OMCs. This surge is largely blamed on the sharp depreciation of the Cedi against the USD since the beginning of the year. Since January, the Cedi has lost about GHS1 to the USD. This, coupled with the international supply chain bottlenecks, continues to drive the pump prices of crude and other petroleum products.

Pump prices for diesel have risen above GHS14/Ltr for the first time since February 2023. In Q1 of 2023, the Cedi depreciated significantly against the USD due to the decline in the BOG foreign exchange reserves. As a result, pump prices for petroleum products escalated significantly. However, the approval of the IMF loan facility to Ghana curtailed the sharp depreciation of the Cedi and has since lowered pump prices to sell below GHS14/Ltr. The recent depreciation of the cedi has again forced the diesel pump price to surge above the GHS14/Ltr mark. Diesel currently sells at an average of GHS14.0590/Ltr, compared to GHS12.7450/Ltr and GHS10.2740/Ltr in 2023 and 2022, respectively.

Going into the second quarter of 2024, pump prices of petrol, diesel, and LPG are expected to increase given the surge in global demand, cuts in production by some OPEC+ nations, attacks on some refineries in Russia by Ukraine, and the continued depreciation of the Cedi in the 16th to 31st March pricing window due to the sharp depreciation of the Cedi against the US Dollar.