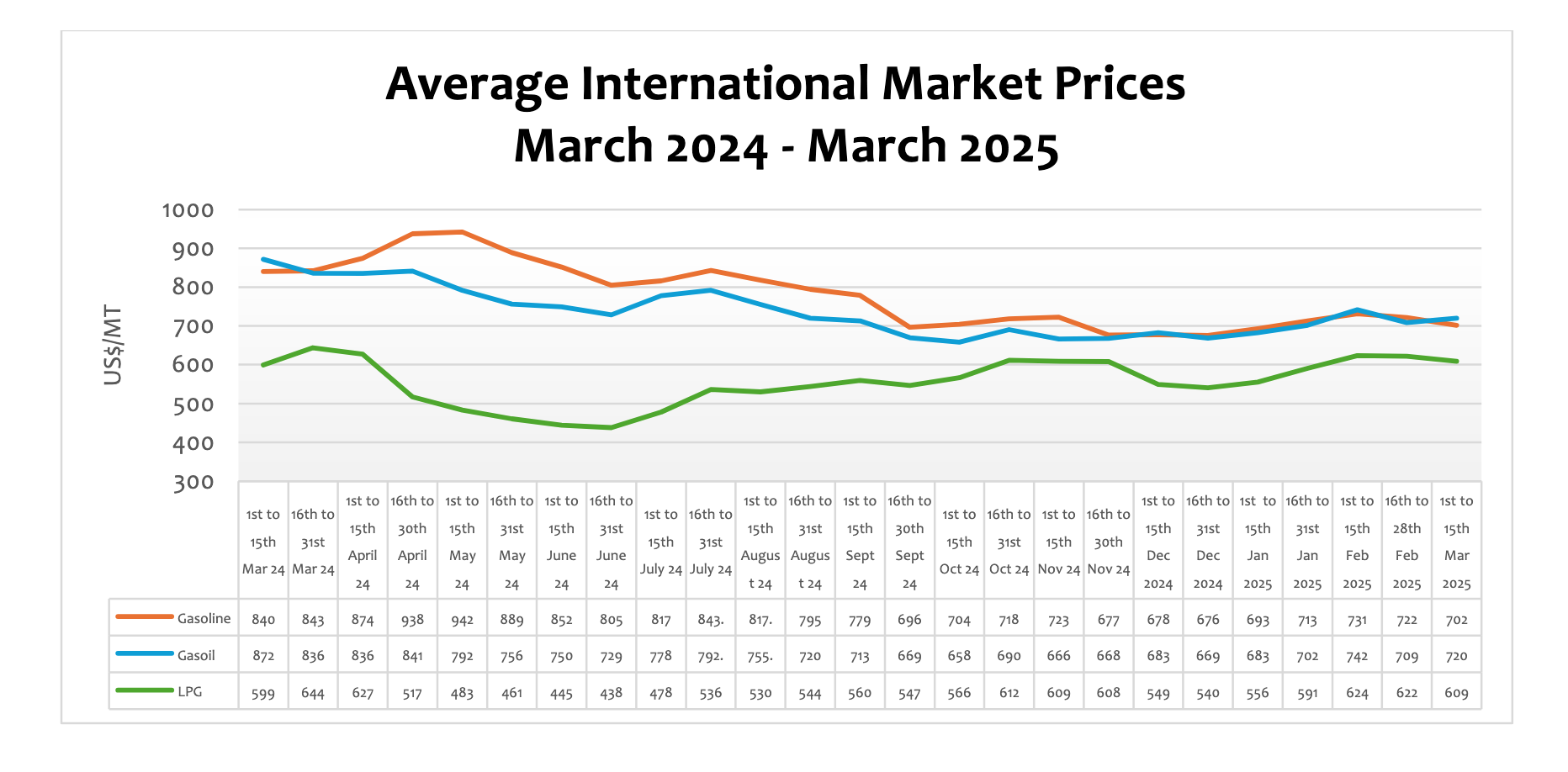

Crude Oil and Refined Products Market Review and Outlook

The global demand for crude and petroleum products fell slightly in the window under review due to the US Administration’s tariff war policies which affected the supply chain dynamics and extended inflationary pressures within the oil markets, contributing to market volatility.. Even though crude oil prices have trended upwards in the past 4 months propelled by high demand, colder weather across the Northern Hemisphere, and optimistic global economic growth, crude prices fell in the window under review due to uncertainty in US foreign policy. The U.S. Energy Information Administration (EIA) projects a steady increase in U.S. crude oil production over the next two years, with output expected to average 13.59 million barrels per day (b/d) in 2025 and 13.73 million b/d in 2026. . It is estimated that global crude demand will also rise from an annual growth of 940 kb/d in 2024 to 1.05 mb/d in 2025, with the US crude oil production projected to significantly increase global supply.

According to CITAC Africa, the Trump administration announced on 1st February 2025, 25% tariffs on all imports from Canada and Mexico, as well as a 10% tariff on imports from China, which potentially disrupted US refinery runs and product exports. On February 4, the Trump administration imposed additional sanctions on Iran, aiming to restrict the country’s nuclear program. It also sanctioned certain entities and vessels involved in transporting Iranian crude oil to China, a measure that could potentially lower Chinese refinery runs and reduce product exports.

Global market prices of crude, petrol, and LPG declined by 1.88%, 1.73%, and 2.11 respectively, while diesel increased by 1.62% due to the recent developments with the US sanctions on its trading partners.

FuFeX30 and Spot Rates

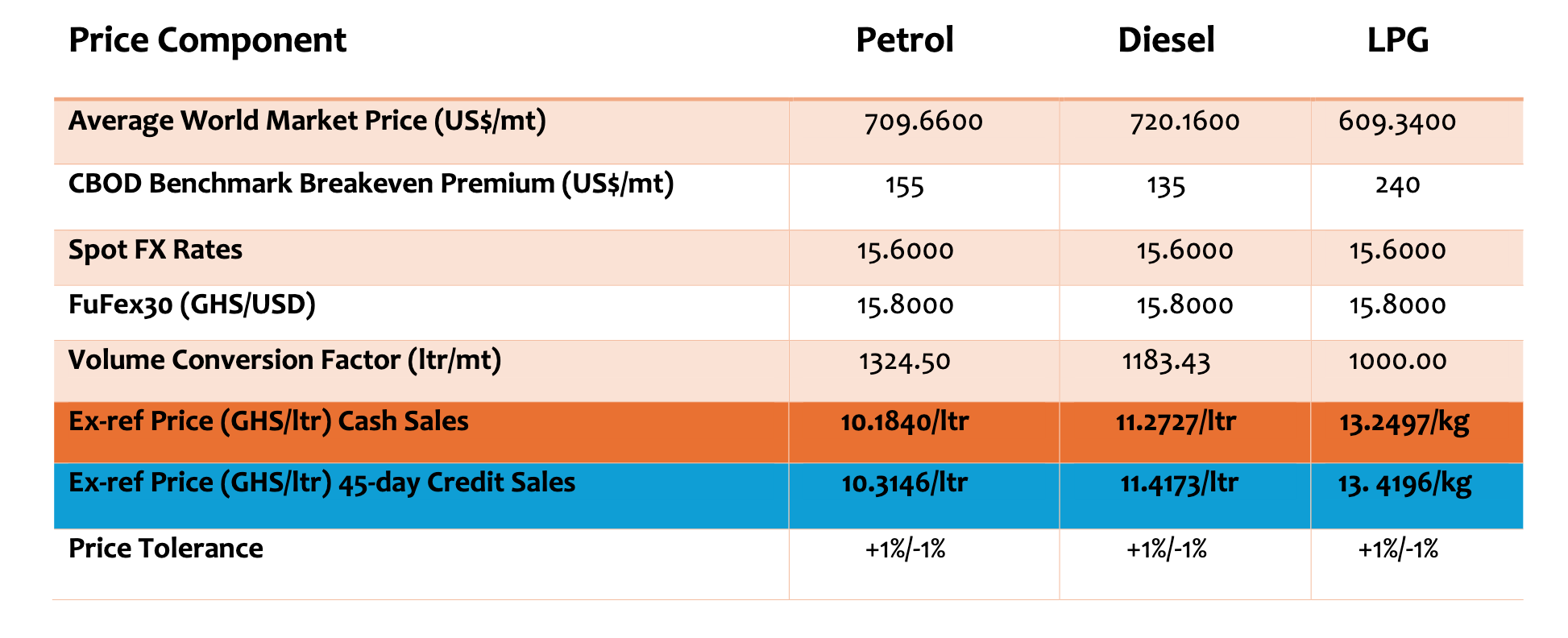

The Fufex30[1] for the Second selling window of February (1st to 15th March 2025) is estimated at GHS15.8000/USD, while the applicable spot rate for cash sales is GHS15.6000/USD based on quotations received from oil financing commercial banks.

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.

| SUMMARY REPORT OF BANK OF GHANA FX AUCTIONS TO BIDECs | ||

| Window | Percentage Offered | Auction FX Rate (GHS/USD) |

| 1st to 15th October 2024 | 32% | 15.7994 |

| 16th to 31st October 2024 | 40% | 15.8682 |

| 1st to 15th November 2024 | 26% | 16.3933 |

| 16th to 30th November 2024 | 28% | 16.2094 |

| 1st to 15th December 2024 | 27% | 15.5388 |

| 16th to 31st December 2024 | 26% | 14.8133 |

| 1st to 15th January 2025 | 25% | 14.7690 |

| 16th to 31st January 2025 | 26% | 14.9443 |

| 1st to 15th February 2025 | 20% | 15.4725 |

| 16th to 28th February 2025 | 23% | 15.4684 |

| 1st to 15th March 2025 | 24% | 15.5582 |

The BoG’s biweekly FX auction to BIDECs in the 1st to 15th March 2025 pricing window for the purchase of petroleum products was US$20 million, representing 24% of BIDECs’ bid. The FX rate at which the BoG auctioned to BIDECs rose from GHS14.7690 in January 2025 to GHS15.5582 per USD in the current window, representing a depreciation of 5.34%. It is expected that the government will implement appropriate policy actions to promote the stability of the cedi to ensure stable pump prices.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window, and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 1st to 15th March 2024

Taxes, Levies, and Regulatory Margins

Total taxes, levies, and regulatory margins within the 16th to 28th February 2024 selling window accounted for 21.48%, 21.05%, and 12.25% of the ex-pump prices of petrol, diesel, and LPG, respectively.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) LPG (GHS/KG) | |

| ENERGY DEBT RECOVERY LEVY | 0.49 | 0.49 | 0.41 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRICE STABILISATION & RECOVERY LEVY | 0.16 | 0.14 | 0.14 |

| SANITATION & POLLUTION LEVY | 0.10 | 0.10 | – |

| ENERGY SECTOR RECOVERY LEVY | 0.20 | 0.20 | 0.18 |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.26 | – |

| BOST MARGIN | 0.12 | 0.12 | – |

| FUEL MARKING MARGIN | 0.09 | 0.09 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.90 | 0.90 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 3.27 | 3.25 | 2.11 |

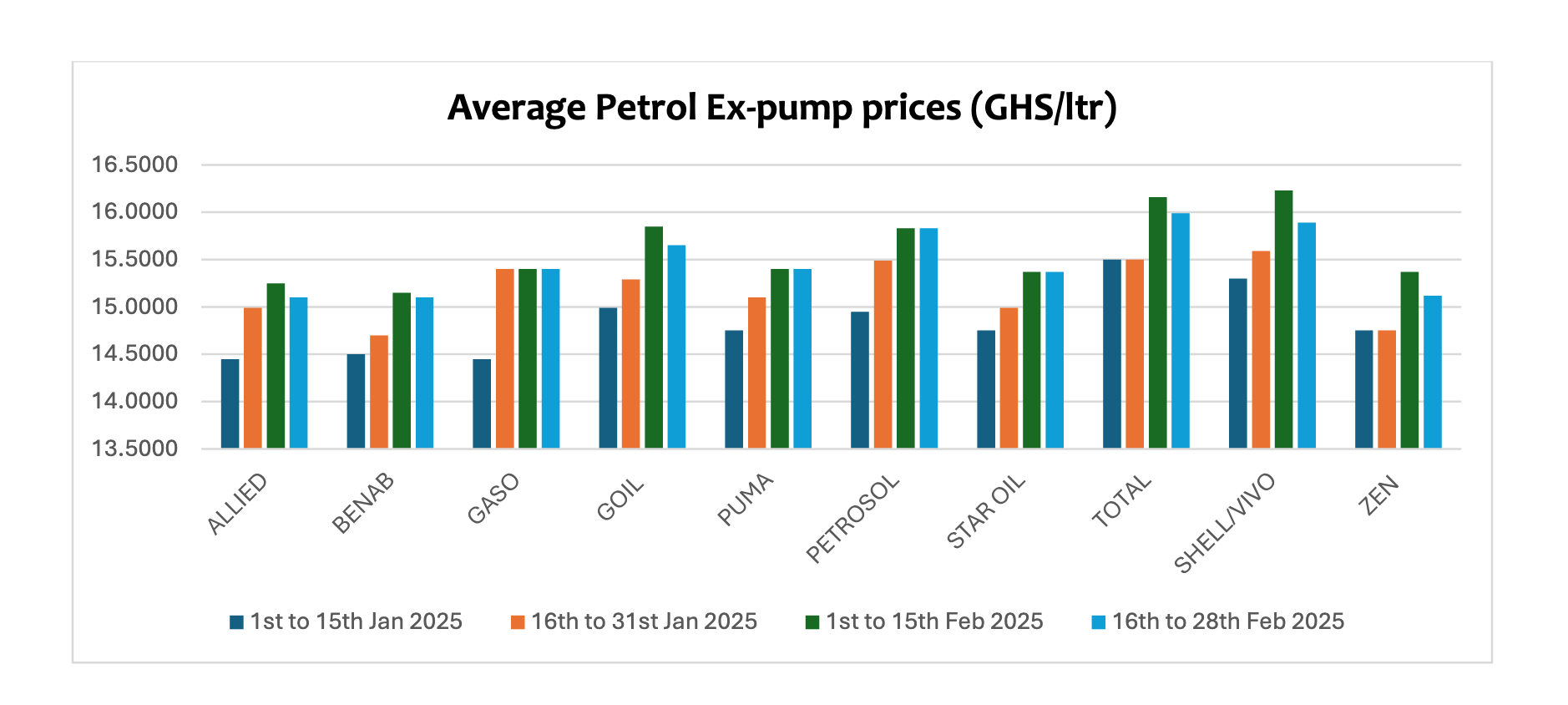

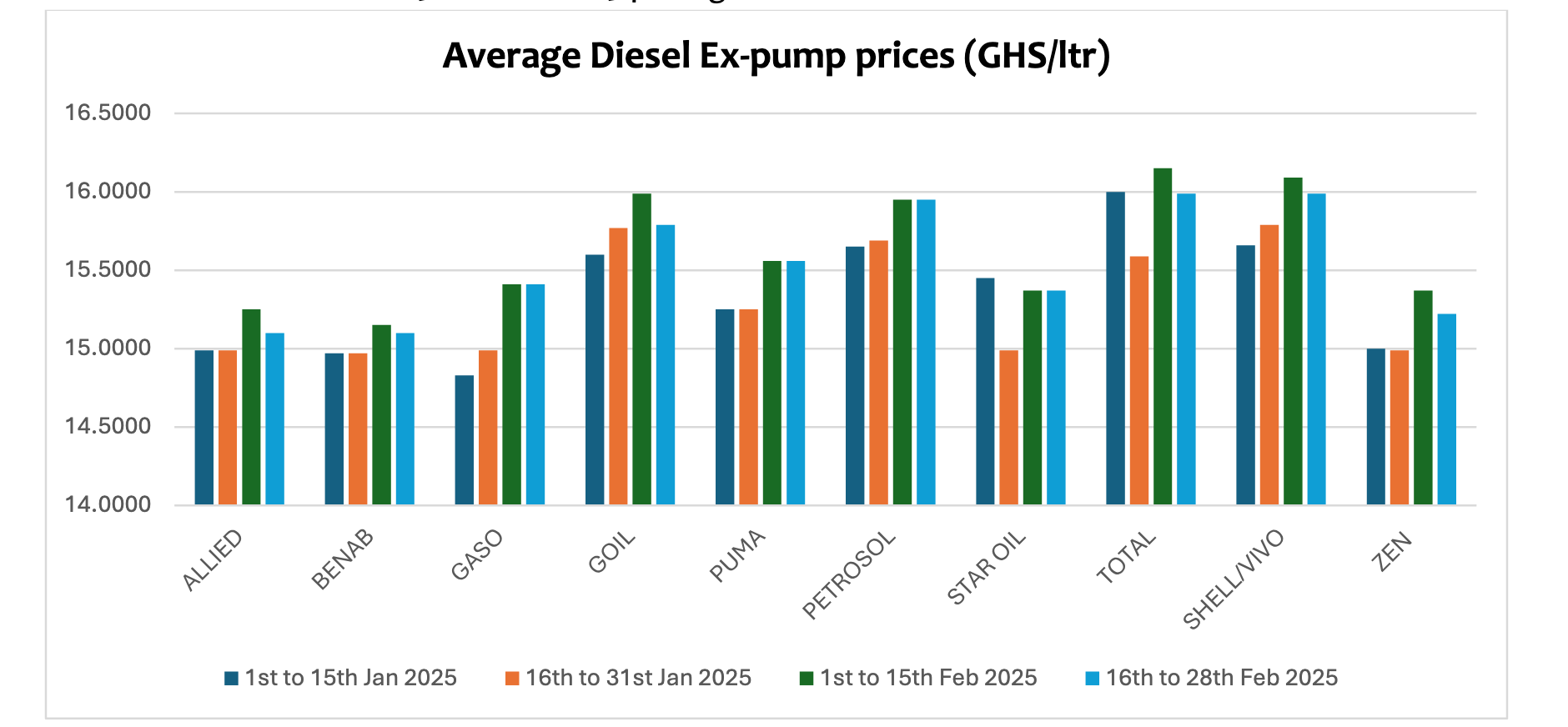

OMC Pricing Performance: 16th to 28th February 2025

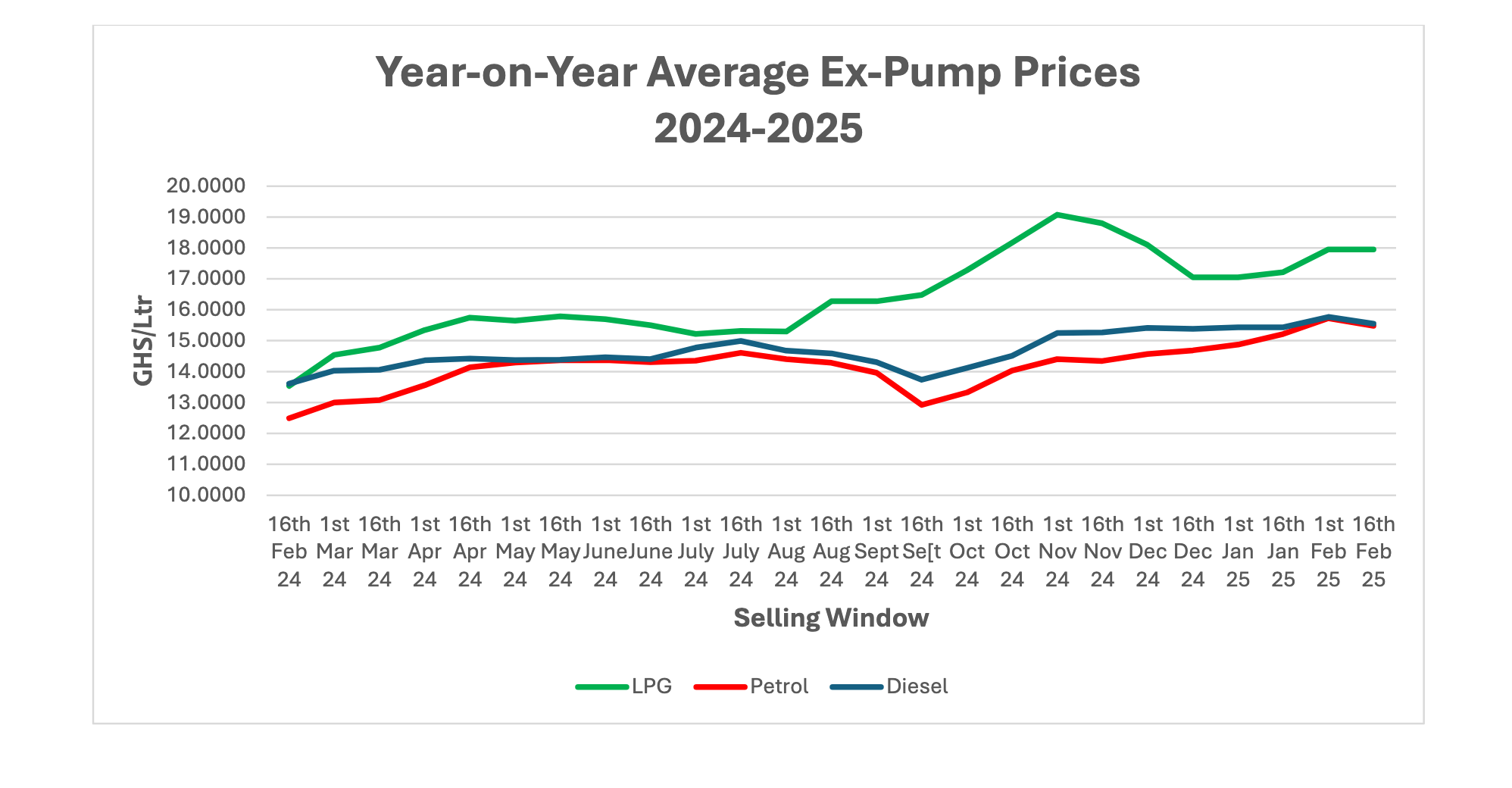

Petroleum products consumption increased significantly across all regions in 2024 by an average of about 17.44%. This has been propelled by increased economic activities and favourable post-COVID-19 recovery in the country despite the adverse impact of the sharp depreciation of the cedi in recent years. The region with the largest consumption was the Greater Accra region with about 1.504mn MT while the Volta region had the lowest consumption of 171,016 MT. Goil PLC continued its dominance of the OMC space with a market share of 11.73% followed by Star Oil, Vivo Energy, Total Energies PLC, and Zen at 9.69%, 7.63%, 6.42%, and 6.19% respectively. Pump prices of petroleum products rose significantly in 2024 due to the sharp depreciation of the cedi against its major trading currency. The cedi depreciated significantly in 2024 resulting in about a 10% increase in the average pump price of petrol and diesel.

The rising pump prices continue to impact transport fares, food prices, the adoption of LPG, and the general cost of living. LPG consumption fell by about 12% in 2022 mainly due to rising costs driven by Exchange rate depreciation. The GHS/USD exchange rate, which is the major drive of pump prices rose to about 16 in November 2024. It is expected government policy and BOG’s intervention will continue to firm up the cedi against its major trading currencies in 2025.

In the pricing window under review, pump prices of petrol fell by 0.71% after increasing by over 3.30% in the previous window. Pump prices of petrol are currently around 23.91% on a year-on-year basis. Given the current decline in global prices and the relative depreciation of the cedi, petrol prices are expected to remain stable in the 1st to 15th March 2025 pricing window.

Pump prices of diesel also declined slightly by 0.52% after increasing by about 2.20% in the window in the previous window. Pump prices of diesel are about 14.21% higher on a year-on-year basis.

As global demand is expected to rise in Q1 2025, pump prices are projected to range above GHS13/Ltr. However, this projection is highly dependent on the performance of the cedi against its main trading currencies, especially the US dollar given that global prices are projected to decline in March.