Crude and Refined Products Price Review and Outlook

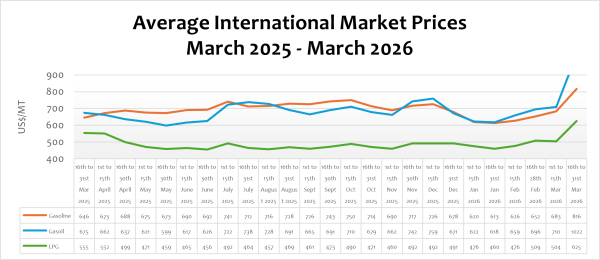

International prices of crude oil have surged significantly due to the ongoing US/Israel-Iran war in the Middle East, despite the decision by the International Energy Agency (IEA) and the G7 countries to release a record volume of oil stockpiles to help mitigate potential supply disruptions. Crude oil prices, in particular, surged to their highest level since 2022, reaching approximately US$120/bbl at the peak of the tensions before moderating to an average of US$86.5/bbl. Crude oil price have risen significantly by 40.18% from January to second week in March arising mainly from the ongoing war.

The persistent strikes have also heightened concerns over global oil supply security, with Iran repeatedly threatening to close the Strait of Hormuz, a critical shipping route through which roughly 20% of global oil consumption and nearly 30% of the world’s seaborne crude and petroleum product trade flows. This has also unexpectedly escalated attacks on oil refineries and storage infrastructure across the Middle East. According to Reuters, three oil vessels were reportedly attacked by Iran in the Strait of Hormuz, further intensifying fears of supply disruptions in the region.

Current crude oil prices also reflect a significant geopolitical risk premium estimated at about US$20/bbl, largely driven by attacks on vessesl within the Persian Gulf. Consequently, international prices of refined petroleum products have recorded sharp increases. Prices of petrol, diesel, LPG, and ATK surged by approximately 19.41%, 43.94%, 23.96%, and 63.61%, respectively. Despite the recent global hikes, petrol, diesel, and LPG are down on a year on year basis by 24.61%, 18.01%, and 25.54%, respectively.

Following the surge in crude prices, OPEC has announced its intention to increase output by approximately 137,000 bpd in March and April 2026, in an effort to stabilize the market. Petroleum product pump prices in Ghana are expected to rise proportionately in the upcoming pricing window of 16th to 31st March 2026.

FuFeX30 and Spot Rates

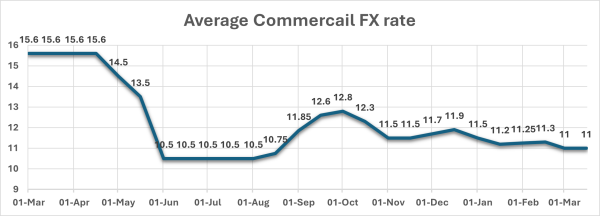

The Fufex30[1] for the first selling window of March (16th to 31st March 2026) is estimated at GHS11.0000/USD, based on quotations received from oil-financing commercial banks. Moreover, the applicable spot rate for cash sales is estimated at GHS10.8000/USD based on quotations from oil-financing commercial banks, representing an appreciation of 2%.

The graph above shows that although the cedi recorded significant appreciation in 2025, persistent volatility continues to undermine effective business planning. A strong and stable currency delivers sustained benefits to the broader economy, particularly for petroleum products, which are predominantly imported and therefore highly sensitive to exchange rate fluctuations. We therefore urge government and policy makers to adopt policies to curtail persistence volatilities of the cedi.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 16th to 31st March 2026

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 816.1400 | 1021.6100 | 625.2800 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 150 | 150 | 200 |

| Spot FX Rates | 10.8000 | 10.8000 | 10.8000 |

| FuFex30 (GHS/USD) | 11.0000 | 11.0000 | 11.0000 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 7.8779/ltr | 10.6921/ltr | 8.9130/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 8.0238/ltr | 10.8901/ltr | 9.0781/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

Total taxes, levies, and regulatory margins within the 1st to 15th March 2026 selling window accounted for about 39.45%, 35.27%, and 16.52% of the ex-pump prices of petrol, diesel, and LPG, respectively. This data shows that consumers are overburdened with levies on petroleum products.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) | LPG (GHS/KG) |

| ENERGY SECTOR SHORTFALL AND DEBT REPAYMENT LEVY | 1.95 | 1.93 | 0.73 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.26 | – |

| BOST MARGIN | 0.12 | 0.12 | – |

| FUEL MARKING MARGIN | 0.09 | 0.09 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.90 | 0.90 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 4.27 | 4.25 | 2.11 |

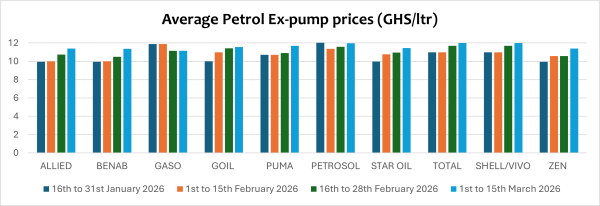

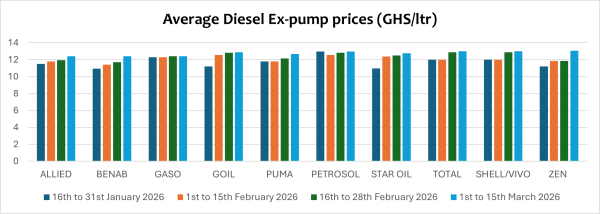

OMC Pricing Performance: 1st to 15th March 2026

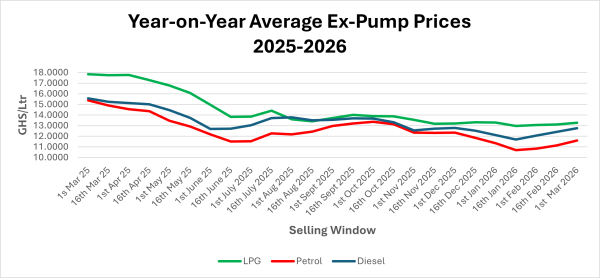

Generally, pump prices of petroleum products in Ghana have trended downward since around April 2025, largely driven by the appreciation of the Ghana cedi and declining international prices of crude oil and refined petroleum products. These developments translated into lower ex-pump prices across several pricing windows, with petrol falling below GHs10/Ltr and diesel below GHs12/Ltr at some retail outlets in January 2026. The sustained reductions provided notable relief to consumers, contributed to a decline in transport fares, and helped ease the inflationary pressures within the economy.

However, developments in the global oil market have begun to exert upward pressure on domestic fuel prices. Escalating geopolitical tensions in the Middle East have pushed international crude oil prices higher, which has gradually filtered into the local petroleum pricing structure. Ghana, like many African countries, remains heavily reliant on imported refined petroleum products, making domestic pump prices highly sensitive to global supply disruptions and geopolitical risks.

The recent surge in global oil prices has been attributed to heightened tensions involving the US/Israel and Iran, particularly concerns surrounding possible disruptions to shipping routes in the Strait of Hormuz and attacks on Oil infratructurre and oil vessels in the Persian Gulf. As a result, the gains recorded earlier in the year from falling international prices and a stronger cedi are gradually being eroded, leading to increases in pump prices across recent pricing windows.

In the window under review, pump prices of petrol rose by about 4.30% due to the surge in international prices arising from the escalating US/Israel and Iran war in the Middle East, which has escalated to the Gulf countries. On a year-on-year basis, pump prices of petrol are down by about 24.63%. However, pump prices are up by about 2.37% compared to January of this year.

Similarly, pump prices of diesel also rose by an average of about 2.88% in the window under review due to similar factors. Compared to the same period last year, pump prices of diesel are down by 20.30% and up by 5.40% compared to January 2026. LPG, however, rose slightly by 1.25% due to international market factors.

In the coming window of 16th to 31st March, pump prices are expected to experience further upward adjustments if geopolitical tensions persist and international crude prices remain elevated. However, market analysts indicate that any significant increase may be moderated if major oil-producing countries increase supply or release strategic reserves to stabilise the global oil market.

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.