Crude Oil and Refined Products Market Review and Outlook

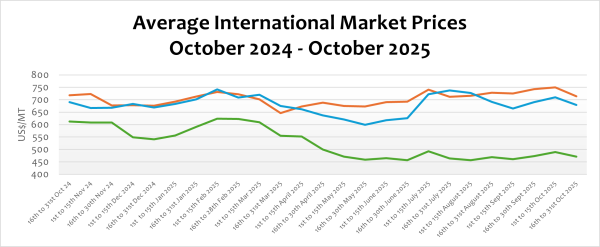

During the pricing window under review, the international market price of crude oil declined by about 2.03% compared to the previous window. Increased production from both OPEC and non-OPEC member countries largely drove the price reduction, resulting in a higher supply relative to demand. It has been projected by the International Energy Agency (IEA) that the global crude oil surplus will average about 3.6 million barrels per day in the last quarter of the year, reflecting strong supply growth relative to demand.

Consequently, prices of refined petroleum products on the international market recorded notable declines. Petrol, diesel, aviation turbine kerosene (ATK), and liquefied petroleum gas (LPG) fell by approximately 4.85%, 4.38%, 2.72%, and 3.78%, respectively. The downward trend in refined product prices is further supported by slower economic growth in major consuming regions such as China and the Eurozone, where tightening monetary policies and subdued manufacturing output continue to dampen fuel demand.

The easing of geopolitical tensions, particularly the anticipated Israel–Hamas ceasefire, is also expected to enhance crude supply from the Middle East, further exerting downward pressure on prices. On the demand side, global consumption is expected to weaken as the Northern Hemisphere enters the winter season, leading to a seasonal slowdown in transport and industrial activity.

Moreover, market forecasts suggest that crude and refined product prices are likely to experience further moderation in the near term, driven by persistent supply surpluses, reduced geopolitical risks, and weak demand fundamentals as the year draws to a close. The decline in international crude and refined product prices during the current pricing window is expected to exert downward pressure on ex-pump prices of petroleum products on the Ghanaian market.

FuFeX30 and Spot Rates

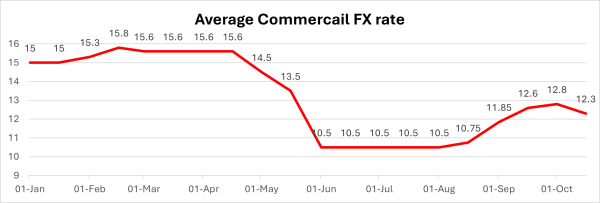

The Fufex30[1] for the second selling window of October (16th to 31st October) is estimated at GHS12.3000/USD, based on quotations from oil financing commercial banks. Moreover, the applicable spot rate for cash sales is estimated at GHS12.0000/USD based on quotations from oil financing commercial banks.

The cedi for the last two months has dropped significantly from about GHS10.50/USD in August to about GHS12.80/USD at the end of September. This sharp depreciation has been a key driver of the surge in pump prices over the period. However, recent significant intervention by the central bank has stabilised the cedi, resulting in a substantial appreciation of the cedi in the second week of October. This will significantly lower pump prices of petroleum products in the coming window.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 16th to 31st October 2025

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 716.3000 | 681.3300 | 472.3000 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 200 | 200 | 255 |

| Spot FX Rates | 12.0000 | 12.0000 | 12.0000 |

| FuFex30 (GHS/USD) | 12.3000 | 12.3000 | 12.3000 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 8.3017/ltr | 8.9367/ltr | 8.7276/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 8.5092/ltr | 9.1601/ltr | 8.9458/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

Total taxes, levies, and regulatory margins within the 1st to 15th October 2025 selling window account for about 31.94%, 31.09%, and 15.52% of the ex-pump prices of petrol, diesel, and LPG, respectively. This data shows that consumers are overburdened with levies on petroleum products.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) | LPG (GHS/KG) |

| ENERGY SECTOR SHORTFALL AND DEBT REPAYMENT LEVY | 1.95 | 1.93 | 0.73 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.26 | – |

| BOST MARGIN | 0.12 | 0.12 | – |

| FUEL MARKING MARGIN | 0.09 | 0.09 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.90 | 0.90 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 4.27 | 4.25 | 2.11 |

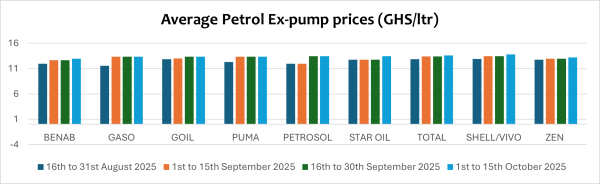

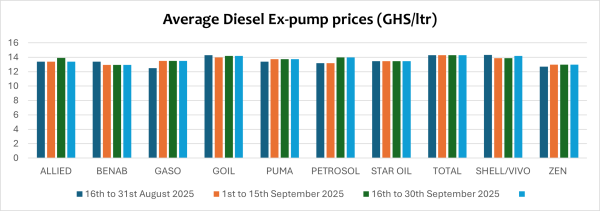

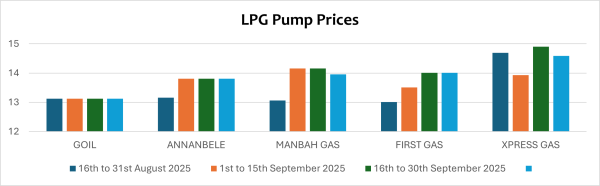

OMC Pricing Performance: 1st to 15th October September 2025

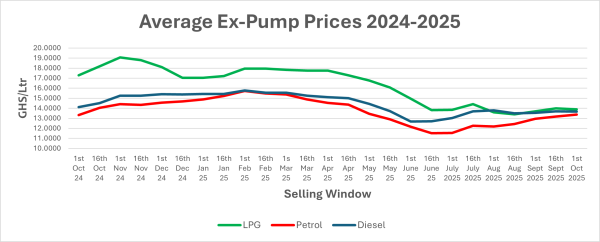

The combined pressures of external market dynamics and domestic currency challenges exerted pressure on the domestic market, leading to a notable escalation in pump prices of petroleum products across the country. This underscores the complex interplay between global events and domestic factors, particularly local currency performance, on the pump prices of petroleum products.

The increase in consumption across advanced and emerging markets exerted upward pressure on international prices, coupled with the depreciation of the Ghana cedi against the US dollar in the past led to the increase in pump prices of petroleum products. The pump price of petrol increased from about GHS11.5110/Ltr to GHS13.3700/Ltr, while diesel rose from GHS12.6000/Ltr to GHS13.6700/Ltr in just one month. These adjustments represent a substantial increase, with potential implications for inflationary trends, transportation costs, and general economic activity.

Due to the depreciation of the cedi in the period and relatively low stocks of petrol, pump prices of petrol rose by about 1.37% to an average of GHS13.3700/Ltr. Compared to January this year, pump prices of petrol are down by about 10.13%.

Average pump prices of diesel declined by 0.15% from GHS13.6910/Ltr to GHS13.6700/Ltr due to the significant fall in the international market price of diesel in the period. LPG also declined by 0.73% from an average of GHS14.000/Kg to GHS13.8980/Kg due to the decline in the international price of LPG.

Due to the significant decline of refined petroleum product prices on the international market and the notable appreciation of the cedi in the current window compared to the previous window, pump prices are expected to decline in the coming window of 16th to 31st October 2025. This trend, if sustained, will provide relief to consumers and support broader price stability within the economy, especially as global demand softens towards the end of the year.

This development underscores the importance of stabilising the domestic currency while exploring long-term measures to cushion the economy against external shocks.

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.