Crude Oil and Refined Products Market Review and Outlook

Global crude oil prices fell sharply in 2025 driven by economic and geopolitical factors that affected demand and supply dynamics in the international market. As a result, average crude oil prices declined by about 14% in 2025 from an average of USD81.03/bbl in 2024 to an average of USD69.70/bbl in 2025.

On the supply side, some of the various factors that contributed to the decline in crude prices in 2025 included the retaliatory tariff impositions between the US and China during the period, the Israel-Iran conflict, and the increase in production by other OPEC and non-OPEC countries. The demand side was weakened by the slower-than-expected economic growth, increasing adoption of electronic vehicles (EVs), and lackluster demand in Asia and Europe.

On the supply side, some of the various factors that contributed to the decline in crude prices in 2025 included the retaliatory tariff impositions between the US and China during the period, the Israel-Iran conflict, and the increase in production by other OPEC and non-OPEC countries. The demand side was weakened by the slower-than-expected economic growth, increasing adoption of electronic vehicles (EVs), and lackluster demand in Asia and Europe.

The US Energy Information Administration (EIA) projected that global supply was to potentially increase to about 104.8mn b/d in 2025, driven mainly by supply from the non-OPEC+ nations, thereby impacting refined products.

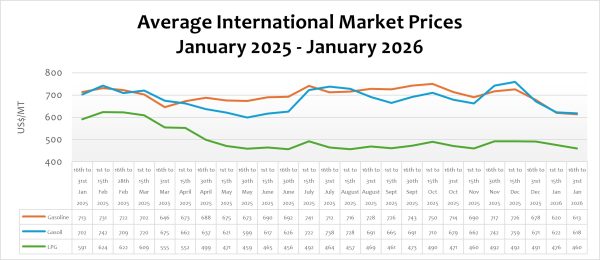

In the refined product space, petrol, diesel, and LPG declined on average by about 11.10%, 9.08% and 7.14% in 2025. The decline was largely driven by the increased crude supply and the dive in global demand, especially from China and Europe. According to CITAC Africa, the global demand growth has in recent years been slowed down by Top of Form

the acceleration of renewable energy.

In the pricing window under review, the global market prices of petrol, diesel, and LPG decline by 1.07%, 0.68%, and 3.40%, respectively, due to a relatively oversupply in the market and the US capture of the Venezuelan president.

FuFeX30 and Spot Rates

The Fufex30[1] for the second selling window of January (16th to 31st January 2026) is estimated at GHS11.2000/USD, based on quotations received from oil financing commercial banks. Moreover, the applicable spot rate for cash sales is estimated at GHS10.9500/USD based on quotations from oil financing commercial banks.

The cedi began the year 2025 at about GHS15/USD, before rising to about GHS15.80/USD. It, however, declined sharply in the second quarter of the year to GHS10.50/USD. The local currency, although volatile throughout the year, was quite stable throughout the second half of the year. This brought predictability in business planning, resulting in the sustained decline in pump prices from an average of about GHS15.4390/Ltr of diesel in January 2025 to GHS12.5350 in December 2025.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window, and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 16th to 31st January 2026

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 613.3900 | 617.6900 | 459.5000 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 200 | 200 | 250 |

| Spot FX Rates | 10.9500 | 10.9500 | 10.9500 |

| FuFex30 (GHS/USD) | 11.2000 | 11.2000 | 11.2000 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 6.7245/ltr | 7.5659/ltr | 7.8238/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 6.8780/ltr | 7.7386/ltr | 8.0024/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

Total taxes, levies, and regulatory margins within the 1st to 15th January 2026 selling window accounted for about 37.68%, 35.12%, and 16.22% of the ex-pump prices of petrol, diesel, and LPG, respectively. This shows that consumers are overburdened with levies on petroleum products.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) | LPG (GHS/KG) |

| ENERGY SECTOR SHORTFALL AND DEBT REPAYMENT LEVY | 1.95 | 1.93 | 0.73 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.26 | – |

| BOST MARGIN | 0.12 | 0.12 | – |

| FUEL MARKING MARGIN | 0.09 | 0.09 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.90 | 0.90 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 4.27 | 4.25 | 2.11 |

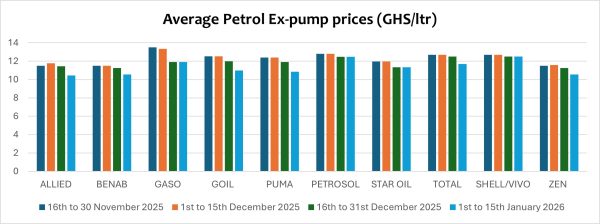

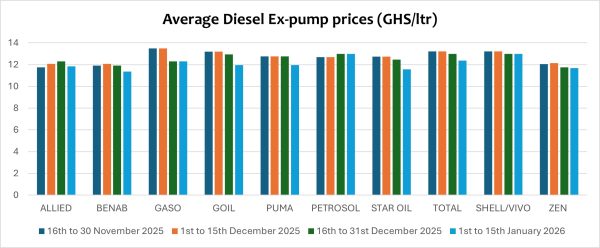

OMC Pricing Performance: 1st to 15th January 2026

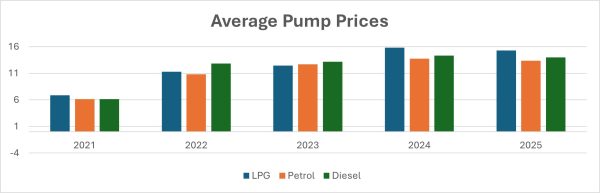

Although the pump price of refined petroleum products declined slightly in 2025 compared to the previous year, pump prices have remained relatively higher compared to 2021 and 2022 prices. This slight decline is largely attributed to the significant appreciation of the cedi against the USD within the period and the sharp fall of international prices of crude and petroleum products. Pump prices of petroleum products rose in 2024 due to the sharp depreciation of the cedi against its major trading currencies. The cedi depreciated by about 40.88% from January to December 2024, resulting in an about 10% increase in the average pump price.

However, the significant appreciation of the cedi against its trading partners in 2025 led to a drop in the pump prices. This brought respite to consumers and motorist, leading to the reduction and transports fares as well as improving LPG adoption.

The GHS/USD exchange rate declined from GHS15.10 to GHS10.50 due to various macroeconomic interventions by the government and the Bank of Ghana. Moreover, the international price of crude oil also declined by about 14% due to increased production by both OPEC and Non-OPEC nations.

Pump prices of petrol have declined by about 2.76% on average. On a year-on-year basis, pump prices of petrol are down by about 23.80%. Given the relative stability of the cedi, petrol prices are expected to remain stable in 2026, contingent on the stability of global geopolitical and economic circumstances.

Pump prices of diesel also declined by an average of about 2.41% in 2025. Compared to the same period last year, pump prices of diesel are down by 21.63%. Diesel is currently being sold below GHS12 per liter among some OMCs.

It is expected that the global market price of crude and petroleum products will continue to decline due to the increasing production of crude. As a result, we project pump prices in 2026 to fall below 2025 levels due to expectations of an improvement in the performance of the GHS/USD rate.

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.