Crude Oil and Refined Products Market Review and Outlook

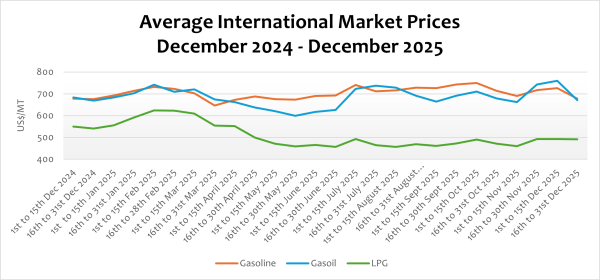

Crude oil prices on the global market, on average, declined by about 7.14% in quarter four (Q4) 2025 compared to quarter three (Q3) 2025. The drop has been attributed to the rising global production by both OPEC and non-OPEC countries. According to Reuters, oil surpluses in 2025 are expected to widen further into 2026 and 2027, as global oil supply is projected to outpace demand, expanding at three times the rate of demand growth through 2026. Crude Oil prices have largely been on a downward trend compared to last year. Compared to crude oil prices in Q4 2024, crude oil prices are down by about 12.95%. This downward trend corroborates IEA’s projection that world oil supply was set to rise by 3.1 mb/d in 2025 and 2.5 mb/d in 2026 on average to reach 108.7 mb/d.”

On the demand side, IEA projects global oil demand to rise by 830 kb/d in 2025 owing to stronger macroeconomic performance and improved trade flows across the globe. The demand growth has been largely influenced by the tariff agreement between the US and China, as well as higher oil demand in China and OECD countries.

The refined petroleum product space witnessed international prices falling significantly within the period by about 6.55% and 11.67% respectively for petrol and diesel, and marginally by about 0.22% for LPG. This is in line with the downward trend of crude oil prices and the high oil inventories being recorded among global producers in Q4.

We anticipate global crude oil and refined product prices to maintain a relatively bullish trajectory, supported by steady demand from key Asian markets and persistent geopolitical tensions. Nonetheless, expected increases in supply from both OPEC and non-OPEC producers, along with seasonal demand slowdowns in certain regions, could cap any significant upward movement in prices.

FuFeX30 and Spot Rates

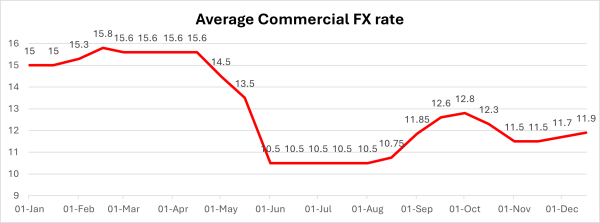

The Fufex30[1] for the second selling window of December (16th to 31st December) is estimated at GHS11.9000/USD, based on quotations from oil financing commercial banks. Moreover, the applicable spot rate for cash sales is estimated at GHS11.6000/USD based on quotations from oil financing commercial banks.

Although the cedi has been relatively stable this year compared to last year 2024, pockets of volatility impacted business within the period. It is expected that the cedi will continue to hold strongly against the USD in December.

The Ex-Refinery Price Indicator (Xpi)

The Ex-ref price indicator (Xpi) is computed using the referenced international market prices usually adopted by BIDECs, factoring in the CBOD economic breakeven benchmark premium for a given window and converting from USD/mt to GHS/ltr using the Fufex30 for sales on credit and the spot FX rate for sales on cash.

Ex-ref Price Effective 16th to 31st December 2025

| Price Component | Petrol | Diesel | LPG |

| Average World Market Price (US$/mt) | 678.1100 | 670.6600 | 491.4100 |

| CBOD Benchmark Breakeven Premium (US$/mt) | 200 | 200 | 255 |

| Spot FX Rates | 11.6000 | 11.6000 | 11.6000 |

| FuFex30 (GHS/USD) | 11.9000 | 11.9000 | 11.9000 |

| Volume Conversion Factor (ltr/mt) | 1324.50 | 1183.43 | 1000.00 |

| Ex-ref Price (GHS/ltr) Cash Sales | 7.6905/ltr | 8.5342/ltr | 8.6584/kg |

| Ex-ref Price (GHS/ltr) 45-day Credit Sales | 7.8894/ltr | 8.7549/ltr | 8.8823/kg |

| Price Tolerance | +1%/-1% | +1%/-1% | +1%/-1% |

Taxes, Levies, and Regulatory Margins

Total taxes, levies, and regulatory margins within the 1st to 15th December 2025 selling window account for about 34.63%, 33.30%, and 16.35% of the ex-pump prices of petrol, diesel, and LPG, respectively. This shows that consumers are overburdened with levies on petroleum products.

| TRM Components | Petrol (GHS/ltr) | Diesel (GHS/ltr) | LPG (GHS/KG) |

| ENERGY SECTOR SHORTFALL AND DEBT REPAYMENT LEVY | 1.95 | 1.93 | 0.73 |

| ROAD FUND LEVY | 0.48 | 0.48 | – |

| ENERGY FUND LEVY | 0.01 | 0.01 | – |

| PRIMARY DISTRIBUTION MARGIN | 0.26 | 0.26 | – |

| BOST MARGIN | 0.12 | 0.12 | – |

| FUEL MARKING MARGIN | 0.09 | 0.09 | – |

| SPECIAL PETROLEUM TAX | 0.46 | 0.46 | 0.48 |

| UPPF | 0.90 | 0.90 | 0.85 |

| DISTRIBUTION/PROMOTION MARGIN | – | – | 0.05 |

| TOTAL | 4.27 | 4.25 | 2.11 |

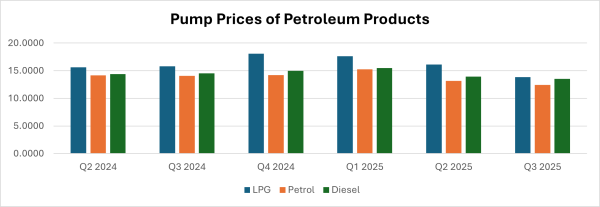

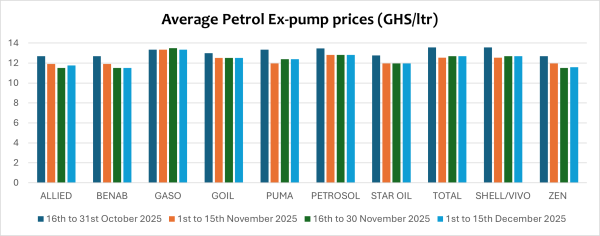

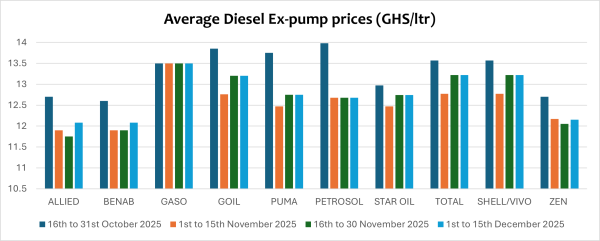

OMC Pricing Performance: 1st to 15th December 2025

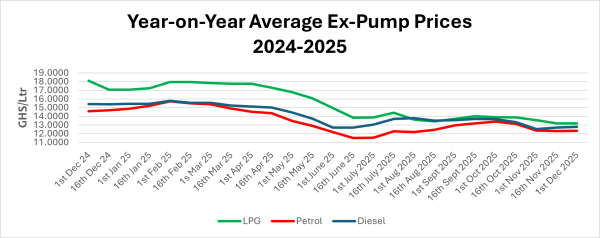

Pump prices of petroleum products have generally been on the decline since January 2025, although prices rose slightly in June and July due to the abrupt surge in international prices occasioned by the Israel-Iran conflict within the period. The 1st to 15th December pricing window saw a slight rise in the price of refined petroleum products at the pumps. The rise was due to the combined effects of international market dynamics and domestic currency performance. This underscores the complex interplay between global events and domestic factors, particularly local currency performance, on the pump prices of petroleum products.

The increase in global crude supply from both OPEC and non-OPEC producers, particularly the United States, Canada, and Brazil, coupled with the appreciation of the Ghana cedi against the US dollar, contributed to a decline in domestic pump prices during the review period.

Petrol pump prices fell below GHS11/Ltr at some OMCs, mainly due to the impact of the FX rate and international prices. On a year-on-year basis, pump prices of petrol are down by 8.50% and down by 17.34% on a year-to-date basis.

Average pump prices of diesel increased by an average of 0.48%, with some OMCs selling below GHS12/Ltr and others above GHS13/Ltr. LPG also rose by 0.15% from an average of GHS13.1360/kg to GHS13.1960/kg due to the surge in the international price of LPG and the slight appreciation of the cedi.

Due to the international market dynamics in relation to crude and refined product prices and the slight depreciation of the cedi against the U.S. dollar this month, it is expected that pump prices will moderately increase or remain unchanged in the last window of the year (16th to 31st December 2025).

[1] The Fufex30 is a 30-day GHS/USD forward fx rate used as a benchmark rate for BIDECs ex-ref price estimations.